When you need extra funds, whether for personal expenses, debt consolidation, or a major purchase, loans are a common solution. But not all loans are created equal. One of the first decisions borrowers face is whether to choose a secured loan or an unsecured loan.

This 2026 guide explains the differences, benefits, risks, and practical scenarios for each type, helping you determine which loan is better for your financial situation.

What Is a Secured Loan?

A secured loan is backed by collateral, meaning you pledge an asset — like a home, car, or savings account — to the lender as security. If you fail to repay, the lender has the right to take possession of the collateral to recover the loan amount.

Common examples of secured loans:

- Mortgage loans (home as collateral)

- Auto loans (car as collateral)

- Home equity loans

- Secured personal loans (backed by savings or investment accounts)

Pros of Secured Loans

- Lower Interest Rates

Because the loan is secured with collateral, lenders face less risk, allowing them to offer lower interest rates than unsecured loans. - Higher Borrowing Limits

Lenders are often willing to approve larger loan amounts because the collateral reduces their potential loss. - Easier Approval

Even borrowers with average or poor credit may qualify if they have valuable collateral.

Cons of Secured Loans

- Risk of Losing Collateral

Failure to repay can result in foreclosure, repossession, or loss of the pledged asset. - Longer Application Process

Lenders may require appraisals or legal documentation to verify collateral value. - Not Ideal for Quick, Small Loans

Secured loans are better for larger amounts and longer-term borrowing.

What Is an Unsecured Loan?

An unsecured loan is not backed by any collateral. Approval is based primarily on creditworthiness, income, and debt-to-income ratio.

Common examples of unsecured loans:

- Personal loans

- Credit cards

- Student loans

- Medical loans

Pros of Unsecured Loans

- No Collateral Needed

You don’t risk your assets — such as your home or car — if you fail to repay (though lenders may send unpaid balances to collections). - Faster Processing

Without collateral verification, unsecured loans are quicker to approve, often within 24–48 hours online. - Flexibility

Funds can be used for almost any purpose — personal, business, or emergency expenses.

Cons of Unsecured Loans

- Higher Interest Rates

Because lenders face more risk, APR is typically higher than secured loans. - Lower Borrowing Limits

Lenders are cautious and may approve smaller loan amounts compared to secured options. - Strict Approval Criteria

Good credit and steady income are often required.

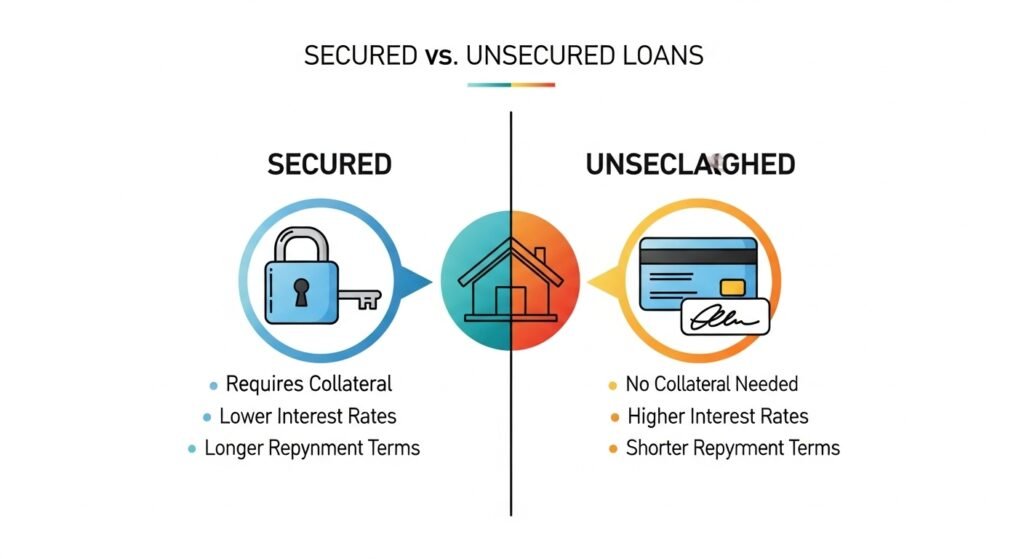

Key Differences Between Secured and Unsecured Loans

| Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral | Required (home, car, savings) | Not required |

| Interest Rate | Lower | Higher |

| Loan Amount | Higher limits | Usually lower |

| Approval Chances | Easier with collateral | Stricter; relies on credit |

| Risk to Assets | High — collateral can be lost | Low — no assets at stake |

| Processing Time | Longer (documentation & verification) | Faster (online or in-person) |

When to Choose a Secured Loan

A secured loan may be better if:

- You need large loan amounts (home, auto, business expansion)

- You want lower interest rates

- You are confident in your ability to repay on time

- You have valuable assets to pledge

Example: Taking a mortgage to buy a house is a secured loan — the house itself is collateral. The risk is justified by the lower interest rate and longer repayment term.

When to Choose an Unsecured Loan

An unsecured loan may be better if:

- You need quick access to cash

- You don’t want to risk personal assets

- The loan amount is moderate or small

- You have good credit and steady income

Example: A $5,000 personal loan for medical bills or debt consolidation is best as an unsecured loan — fast approval and no collateral required.

Factors to Consider Before Choosing a Loan

- Purpose of the Loan

- Large purchases → secured loan

- Short-term emergency → unsecured loan

- Your Credit Score

- Poor credit → secured loan may be easier to obtain

- Good credit → unsecured loan is feasible

- Risk Tolerance

- Comfortable risking collateral → secured loan

- Risk-averse → unsecured loan

- Repayment Ability

- Secure enough cash flow for monthly payments? Choose based on interest rate and loan term.

Tips for Securing the Best Loan in 2026

- Compare Lenders: Online platforms and banks may offer different rates.

- Check APR and Fees: Factor in origination fees, late fees, and prepayment penalties.

- Negotiate Terms: For secured loans, sometimes collateral or repayment terms can be adjusted.

- Consider Hybrid Options: Some lenders offer partially secured loans with flexible terms.

Conclusion

There is no one-size-fits-all answer to “Secured vs Unsecured Loans: Which is better?”

- Secured loans are better for larger amounts, lower interest rates, and borrowers willing to pledge collateral.

- Unsecured loans are better for quick funding, moderate amounts, and borrowers who prefer not to risk assets.

Ultimately, the best choice depends on your financial situation, loan purpose, credit score, and risk tolerance. Carefully weigh interest rates, repayment terms, and potential risks to choose the loan that supports your 2026 financial goals safely.

FAQ – Secured vs Unsecured Loans (2026)

❓ Can I convert an unsecured loan into a secured loan?

Yes — some lenders allow adding collateral to reduce interest rates.

❓ Which loan type has better credit-building potential?

Both can help build credit if you repay on time, but unsecured loans report directly to credit bureaus more frequently.

❓ Are secured loans safer for lenders or borrowers?

Safer for lenders; for borrowers, risk depends on their ability to repay, since default can mean losing collateral.

❓ Is a personal loan usually secured or unsecured?

Most personal loans are unsecured, unless you pledge collateral like a savings account.